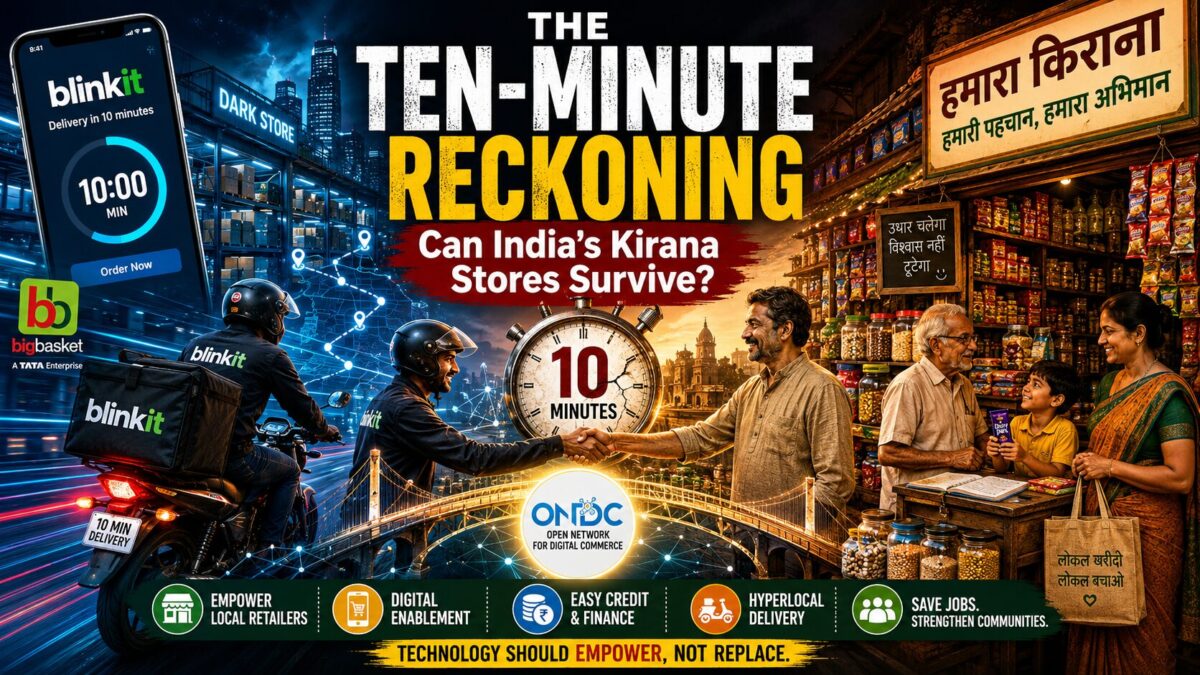

On a narrow lane in any Indian city, the neighbourhood kirana store has always been more than a shop. It is a ledger of trust — a place where credit is extended on memory rather than paperwork, where the shopkeeper knows exactly which brand of atta a household prefers, and where a missing ingredient at 9 pm is never a crisis. That relationship, built over decades, is now being tested by a phone screen and a ten-minute delivery promise. The question this piece sets out to answer is not whether quick commerce is disrupting India’s retail economy — the data leaves no doubt that it is — but how deep that disruption runs, who is right in the increasingly bitter argument about it, and what a workable path forward actually looks like.

I. The Scale of the Shift

India’s quick-commerce sector has gone from a curiosity to a category that rivals organised retail in scale. Industry estimates put the sector’s gross merchandise value at roughly $11–11.5 billion in 2025, and platforms reported combined order volumes of nearly 7.8 million a day by early 2026 — a number that has effectively doubled year-on-year. Projections from Redseer and other trackers see the market expanding five-to-seven-fold by 2030, to somewhere between $60 billion and $83 billion.

Three companies dominate this contest. Blinkit, owned by Eternal (formerly Zomato), has pulled decisively ahead: as of March 2026 it operated more than 2,200 dark stores, processed roughly 25 lakh orders a day, and posted ₹37,779 crore in FY26 revenue — becoming, in the process, larger than its own parent’s food-delivery business. It holds an estimated 45–50% share of the market. Swiggy Instamart and Zepto trail at roughly 20–27% each, both still burning significant cash even as revenues more than double year-on-year. BigBasket’s BB Now, backed by the Tata Group, holds a smaller 5–7% slice, while Amazon Now and Flipkart Minutes have entered aggressively, each crossing 500-plus dark stores in 2026.

What makes this relevant to the kirana question is where this growth is coming from. According to a widely cited Datum Intelligence study, Kirana stores’ collective market share in Indian grocery retail fell from 95% in 2018 to 92.6% in 2023, and is projected to slide further to roughly 89% by 2028. The same research found that 46% of quick-commerce users had cut their spending at kirana shops, that 82% had shifted at least a quarter of their regular kirana purchases online, and that 5% had stopped visiting kirana stores altogether. By the traders’ body CAIT’s own estimate, quick commerce has already captured 25–30% of the business once held by kirana stores — enough, it argues, to push nearly a quarter of India’s roughly 30 million kirana outlets to the brink of closure.

II. Two Competing Data Stories

Here the narrative splits, and a responsible account has to hold both halves.

The disruption case. CAIT’s white paper, released in late 2024 and still the reference point for most policy debate on this issue, makes a sharper argument than “kiranas are losing customers.” It alleges that Blinkit, Instamart, and Zepto together drew in over ₹54,000 crore in foreign direct investment, of which barely 2.5% went into genuine infrastructure — warehouses, cold storage, logistics assets — with the rest funding operating losses and steep discounting. CAIT contends this amounts to predatory pricing subsidised by foreign capital, compounded by exclusive-seller arrangements (it names a handful of preferred vendors that account for the bulk of platform inventory) that box out independent wholesalers, and by a lack of seller-disclosure that it says breaches consumer-protection law. In 2025, the All India Consumer Products Distributors Federation escalated this into a formal petition before the Competition Commission of India, asking for a minimum support price tied to MRP and mandatory price floors on FMCG goods. The CCI itself has since drafted new cost-determination regulations, open for comment, aimed squarely at digital-market predatory pricing.

The “fragmentation, not replacement” case. A more recent Redseer analysis complicates the doomsday framing. It argues that kiranas still command roughly 91% of India’s grocery market today and are likely to retain about 85% by 2030 — a much gentler decline than the “kiranas are dying” narrative suggests. Its case: Indian grocery demand is not a single market but several layered ones. Roughly 200 million households run daily baskets of ₹100–200, shaped by tight income cycles — a segment kiranas are structurally built to serve, given lower cost structures and positive margins even on small tickets. Quick commerce, by contrast, thrives on higher-value, convenience-led urban baskets, and its capital-intensive dark-store model — dependent on dense order volumes in roughly 60–70 cities — simply doesn’t translate to the low-basket, high-frequency economics that sustain a kirana. On this reading, quick commerce is less a kirana-killer than a new demand layer sitting alongside e-commerce and modern retail, absorbing incremental growth as much as existing spend.

Both accounts are consistent with the same underlying fact: the overall Indian grocery market is expanding fast — from an estimated $570 billion in 2023 towards $818 billion by 2028 — so a kirana can lose share of category and still, in absolute rupee terms, hold roughly steady. That distinction matters enormously for how alarmed a shopkeeper in a Tier-2 town should actually be, and it is routinely lost in headline framing.

III. Why the Threat Is Real Regardless of Which Story You Favour

Even the more optimistic reading of the data does not erase three structural pressures on kirana stores:

- Unequal cost of capital. Quick-commerce platforms can absorb years of losses because they are backed by venture and private capital chasing scale, not by weekly cash-flow. A kirana owner cannot sustain a loss-making month, let alone a loss-making year, to win market share.

- Urban concentration, but high visibility. The competitive damage is concentrated in dense metro and Tier-1 markets — the roughly 60–70 cities where dark-store density makes ten-minute delivery viable. But these are also the highest-revenue kiranas, meaning the stores that lose the most are often the ones best positioned to invest in survival — if they choose to.

- The erosion of relational advantages. A kirana’s edge has never been price; it has been the khata (informal credit), personalised stocking, and flexible hours. Quick commerce is now encroaching on convenience and speed — the very ground kiranas used to own uncontested — while offering better prices on branded FMCG goods through first-party inventory deals that most small retailers cannot match.

IV. What a Genuine Solution Looks Like

Given this picture, the useful conversation is not “ban quick commerce” versus “let the market decide,” but a set of concrete interventions that address the actual asymmetries.

1. Enforce existing competition and FDI law, rather than write new slogans. India already prohibits FDI in inventory-led e-commerce and permits it only in the marketplace model. If platforms are functionally running first-party inventory (as Blinkit’s own 2025 shift to direct purchasing suggests) while claiming marketplace status for FDI purposes, that is a compliance question the DPIIT and CCI can act on without new legislation. The CCI’s 2025 draft cost-determination regulations are a step toward giving predatory-pricing complaints a testable, evidence-based standard — that process should be completed and applied, not left to linger.

2. Bring kiranas onto digital rails on their own terms — ONDC, done right. The Open Network for Digital Commerce was built precisely to let small retailers plug into digital discovery and logistics without ceding control to a single platform’s algorithm. Its uptake among kiranas has been slow, held back by patchy onboarding support, thin catalogue depth, and inconsistent last-mile fulfilment. Scaling ONDC for kiranas — with government-subsidised onboarding, POS and inventory digitisation, and integration with existing hyperlocal delivery fleets — would let a shopkeeper offer 20–30 minute delivery under their own brand rather than surrendering the customer relationship entirely.

3. A public, interoperable micro-credit line to replace the khata. The informal credit kiranas extend to loyal households is a genuine competitive asset that no app currently replicates. A structured public-private micro-credit framework — RBI-backed, delivered through public-sector banks in partnership with digital retail networks — could let kirana owners offer instant, small-ticket, buy-now-pay-later credit to regular customers, formalising a trust relationship that has existed informally for generations.

4. Cooperative buying power. Individual kiranas cannot negotiate FMCG pricing the way a platform buying at national scale can. Federated buying groups or franchise-style cooperatives — pooling procurement across clusters of kiranas — can compress the wholesale price gap that currently makes platform pricing look unbeatable on staples.

5. Shelf-space and search-neutrality obligations on large dark-store operators. Two ideas gaining traction in policy circles deserve serious pilot testing: requiring large dark-store networks above a certain footprint to allocate a minimum share of shelf space to independently sourced regional goods (turning a closed warehouse into a shared distribution node), and mandating algorithmic neutrality so that platform-owned private labels and preferred sellers don’t receive automatic default visibility over independent listings. Neither eliminates competition; both would blunt its most extractive edges.

6. Targeted digitisation subsidy, not blanket protectionism. Rather than tariff-style protection for kiranas — which tends to preserve inefficiency rather than resilience — a time-bound subsidy for point-of-sale systems, basic inventory software, and delivery-partner integration would help the roughly 30 million kirana stores modernise the parts of their operation that are genuinely behind, while leaving their relational and locational advantages intact.

V. The Honest Bottom Line

Quick commerce is not going away, and pretending otherwise does kirana owners no favours. Blinkit alone is now bigger than Zomato’s core food-delivery business; the sector as a whole is compounding at 40%-plus annually and has government-recognised staying power. But the CAIT allegations around FDI misuse and predatory pricing are serious enough, and specific enough, that they warrant an actual regulatory verdict rather than indefinite study. And the Redseer counter-argument is a useful corrective to panic — India’s grocery market is large and layered enough that quick commerce, kiranas, and organised retail can plausibly coexist, provided the competitive playing field is genuinely level.

The stores most likely to still be standing in 2030 will not be the ones that out-discount Blinkit — that is a fight they cannot win. They will be the ones that convert trust, credit, and hyperlocal knowledge into a digitally-enabled offering, backed by regulation that prevents scale from curdling into monopoly. The ten-minute economy has arrived. Whether the corner store survives it is now a policy choice as much as a market outcome.

Sources synthesised for this piece include reporting and data from Datum Intelligence, Redseer, the Confederation of All India Traders (CAIT), the Competition Commission of India, NIQ’s Shopper Trends 2024 report, Reuters, Business Standard, Inc42, MediaNama, and company filings from Eternal (Blinkit), Swiggy (Instamart), and Zepto.